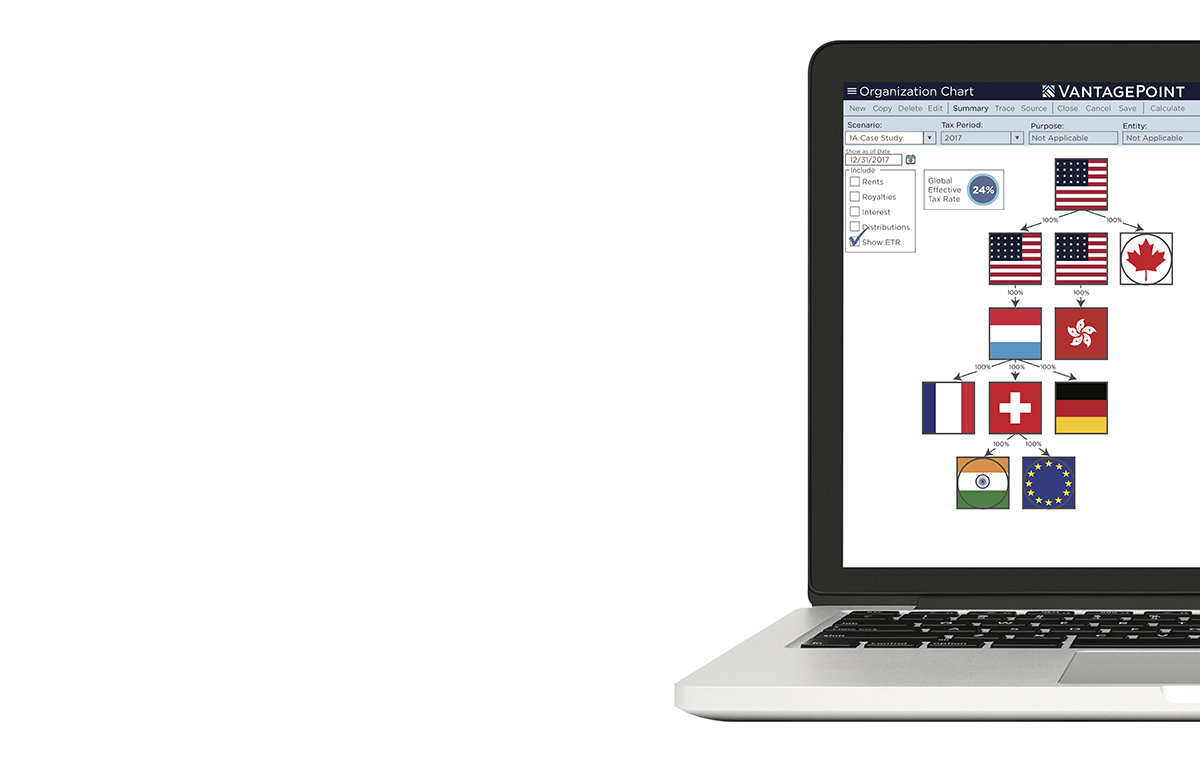

Discover the power of fully integrated Global Tax calculations VantagePoint™ Global Tax Software integrates GILTI, FDII, Sub F, FTC, IC-DISC, BEPS, BEAT, Pillar Two calculations and more. VantagePoint™ is utilized on consulting and co-sourcing engagements and is also available for license. Services Software VantagePoint™ integrates GILTI, FDII, Sub F, FTC, IC-DISC, BEPS, BEAT, and more. It is also available for license. Services Software Resources Pillar Two Boot Camp Register Now 2023 International Tax Boot Camp Program Details 2023 Webinar Series 2023 Webinar Series The most advanced international tax planning and forecasting tool. Unlike traditional compliance software, VantagePoint focuses primarily on global tax optimization, achieving superior overall results. WATCH OVERVIEW VIDEO Events & Insights Sponsorships Schedule a Call Email Subscribe Linkedin Twitter Facebook Youtube Instagram